This has been a regularly repeated theme among many pundits over the past year. Is this assertion supported by data?

Below is the Federal Reserve's most recent report (1Q14) on equity holdings as a percentage of household financial assets (chart from Short Side of Long).

In more than 50 years, equity ownership has only been higher during one quarter in the mid-1960s and the final 15% of the 1982-2000 bull market.

Goldman's data from the end of 2013 includes exposure to international equities. The conclusion is the same.

From the Investment Company Institute June data release: total assets invested in equity mutual funds and ETFs compared to the total assets invested in money market funds (data from Sentimentrader). The relative allocation to equities surpassed the prior highs one year ago.

Assets in Rydex bullish equity funds relative to assets in cash or bearish funds is higher than any time before or since 2000. Rydex total assets are well over $8 billion.

The NYSE releases monthly data on the amount of securities purchased on margin. In June, the amount of margin debt was just 0.4% off the all-time high made in February of this year. As a proportion of market capitalization, it is above highs made in 2000 and 2007.

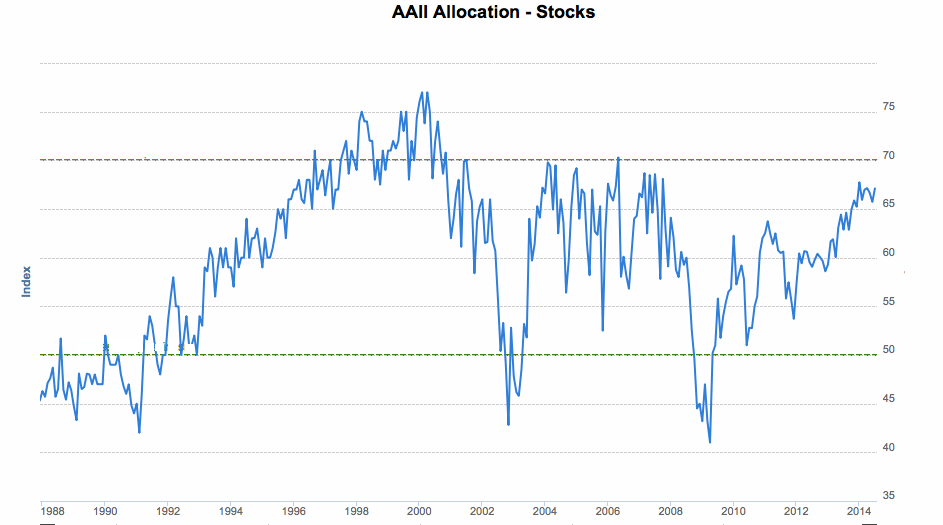

All of the above measure actual assets. In comparison, AAII conducts a voluntary survey among its (retail investor) members each month. In July, members' stated that their asset allocation to cash was at March 2000 lows and 34% below the average (charts from Short Side of Long).

Respondents also reported their equity allocations to be 12% above average and at October 2007 levels.

BAML surveys professional investors managing over $700 billion each month. In July, their equity allocation was the second highest in the survey's 13 year history.

Conclusion: On balance, it doesn't appear that investors have been fighting the rally in equities. Instead, they have fully participated to an extent greater than in 2007 and, by several measures, by an extent greater than in 2000.

This doesn't mean, by itself, that equities are doomed to decline. But it does mean that asset allocation (or sentiment) is not a tailwind to higher prices. What factors will drive equities higher is a valid issue.

Pundits that view the majority of investors as being bearish or sidelined reveal more about their own bias than about the state of the market. As always, aligning opinions with facts is recommended.