Over the past few months. fund managers have been reducing cash, overweighting equities and underweighting bonds to levels that are close to the bullish extremes seen at prior equity tops. Equity exposure in March, for example, was the second highest since the survey began in 2001.

In April, cash levels rose to 4.3%, in the middle of the range. Equity allocations were reduced to 47% overweight; still near the high end of the range. Bonds remained very underweight at a net 50%. Overall, fund managers are still very bullish on risk.

Recall that these are global fund managers, so reducing some risk in the past month reflects deterioration in European and emerging markets, especially China. The US market has been diverging higher. In response, fund managers have raised their overweight bet on the US (and Japan) to 20%. They were 3% underweight the US in January, for comparison. Europe was reduced to 8% underweight in April; it had been 15% overweight in January.

You can see from the data that it should be looked at from a contrarian perspective. Fund managers were overweight EEM more than any other market at the start of the year, and it has been the worst performer so far. They are now becoming bearish EEM, so keep it on your radar. They are also more underweight commodities than at any time since early 2009.

Survey details are below. Read about the March, February and January surveys as well. The charts (from March) are from an excellent post from Short Side of Long (here), a site I recommend bookmarking.

- Cash: Cash balances rose to 4.3% (vs 3.8% in January and February, and 4.1% in December 2012). This is the highest in 6 months. Typical range is 3.5-5%. BAML has a 4.5% contrarian buy level. More on this indicator here and see first chart below.

- Equities: A net 47% are overweight global equities, a 10 percentage point decline from last month (57% in March, 51% in February). March was the second highest equity exposure since the survey began in April 2001. In comparison, it was 35% in December 2012. More on this indicator here and see second chart below.

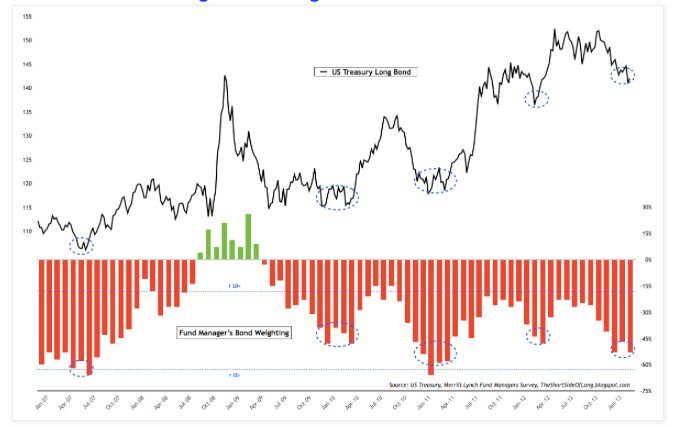

- Bonds: A net 50% are now underweight bonds, a decrease from 53% in March and 47% in February. March was the lowest weighting since May 2011. Third chart below.

- Currencies: Appetite for the dollar is at the highest level in survey history, like March. On the flip side, Yen bearishness is the lowest since February 2002.

- Regions: EEM had been the most favored region (overweight 43% in February) but this fell to +13% in April, the lowest since October 2011. Only 13% expect a stronger Chinese economy in the next year, a massive fall from 71% in January.

- Managers are 20% overweight the US (vs 14% overweight in March and 3% underweight in January), the highest since June 2012.

- They are the most overweight (20%) Japan since 2007 (versus +15% in March, +7% in February and underweight by -20% in December). Every regional fund manager expects the economy to strengthen in the next 12 months.

- Europe was reduced to 8% underweight from 4% overweight in March (+8% in February and +15% in January).

- Sectors: Sector weighting reflect skepticism over emerging markets and concern about EZ.

- Materials weighting is the lowest since 2009.

- Energy weighting is the lowest on record.

- Overall, commodities are 18% underweight (-11% in March, -1% in February), the lowest since January 2009.

- Macro: 49% expect global economy to strengthen next 12 month (61% in March and 59% in February). March was the highest optimism since April 2010. The fall is attributable to Europe; 19% expect strength in the next year, down from 40% in March.

Cash balances are 4.3%, a rise from last month. The one month increase is similar to late 2009 or spring 2011.

A net 47% are overweight equities, higher than 2012 and similar to 2010.

A net 50% are underweight bonds. This is exceptional low.

Commodities are a net 18% underweight, the lowest since January 2009.