On the one hand, fund managers raised cash to a 6 1/2 year high. It hasn't been this high since the height of panic in late 2008. This is normally contrarian bullish.

Note, however, that allocations to equities rose over the past month. Most of the rise in cash came from fund managers further reducing their exposure to emerging markets, Europe, commodities and bonds; allocations to US equities rose.

Moreover, fund managers remain very overweight "risk on" sectors: allocations to discretionary, banks and technology are high and rose further over the past month. Allocations to defensive sectors, like staples, are near all-time lows.

Net, this is not the profile of a market where investors are fearful.

Regionally, allocations to the US and emerging markets are at low levels from which they normally outperform Europe and Japan on a relative basis.

* * *

Among the various ways of measuring investor sentiment, the BAML survey of global fund managers is one of the better as the results reflect how managers are allocated in various asset classes. These managers oversee a combined $600b in assets.

The data should be viewed mostly from a contrarian perspective; that is, when equities fall in price, allocations to cash go higher and allocations to equities go lower as investors become bearish, setting up a buy signal. When prices rise, the opposite occurs, setting up a sell signal.

To this end, fund managers became very bullish in July, September, November and December 2014, and stocks have subsequently sold off each time. Contrariwise, there were some relative bearish extremes reached in August and October 2014 to set up new rallies. We did a recap of this pattern in December (post).

Let's review the highlights from the past month.

Fund managers increased their cash levels to a 6 1/2 year high of 5.5%. This is an extreme and it's normally very bullish for equities. Note that cash levels haven't been much below 4.5% since early 2013.

Fund managers are +42% overweight equities, up from +38% in June. While much has been made about high cash levels signifying risk-aversion, current equity allocations are slightly above the long term mean. This is therefore neutral. A washout low, with investors showing fear, would take place with equity allocations under 15-20%.

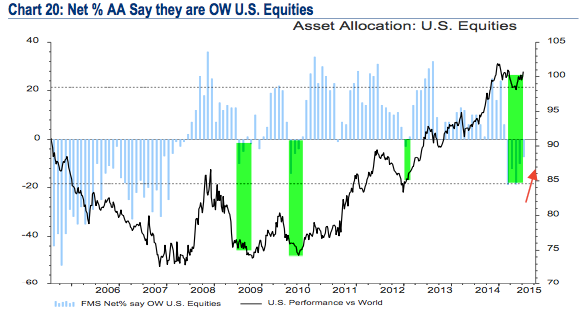

US exposure was -7% underweight in July, an increase from -19% underweight in May. Since then, US equities have outperformed. US equities are still under-owned and should outperform those in Europe and Japan on a relative basis (see below).

Eurozone exposure was +60% overweight in March, the highest in the survey's history. It declined to a still substantial +40% overweight in July from +46% in June. This is still more than 1 standard deviation above the long term mean. Judging from the experience in 2006, European equities are likely to continue to underperform.

{kind=link}

Eurozone exposure was +60% overweight in March, the highest in the survey's history. It declined to a still substantial +40% overweight in July from +46% in June. This is still more than 1 standard deviation above the long term mean. Judging from the experience in 2006, European equities are likely to continue to underperform.

Allocations to Japan stayed near the highs of the last few months (+37% overweight). Allocations the past 9 months haven't been this high since April 2006. This is still more than 1 standard deviation above the long term mean.

Fund managers dropped to -20% underweight emerging markets, almost 2 standard deviations below the mean and at a 16 month low. This is where bottoms tend to form.

Fund managers are -60% underweight bonds, almost 1 standard deviation below the long term mean. Bonds continue to be the most underweighted asset class and this, in large part, explains why cash balances have not been lower that 4.5% in two years. For comparison, managers were -38% underweight in May 2013 before the large fall in bond prices.

Allocations to commodities fell to -22% underweight from -11% underweight in June. This is 1.3 standard deviations below the long term mean.

Globally, managers are not just overweight equity and underweight bonds, they are overweight the highest beta equities (technology, discretionary, banks). The largest underweights are in staples and energy.

In April, the global overweight in discretionary stocks was the highest since the survey began. It is still more than 2 standard deviations above the long term mean. Note that discretionary stocks have underperformed since 1Q15.

Similarly, the global overweight in banks is the highest in the survey's history and well over 2 standard deviations above the long term mean.

In the US, pharma (biotech), banks and tech are the most favored sectors. This has been the case for many months. Utilities, staples, telecoms (defensives) remain underweighted.

In summary: While the high levels of cash are normally very bullish, it's not accurate to say that it represents fear on the part of fund managers. In the past month, equity allocations have increased, as have their allocations to higher-risk cyclicals. Cash is low because allocations fell for emerging markets, Europe commodities and bonds.

Survey details are below.

- Cash (+5.5%): Cash balances rose to 5.5% from 4.9%. This is the highest level since December 2008. Typical range is 3.5-5%. BAML has a 4.5% contrarian buy level but we consider over 5% to be a better signal. More on this indicator here.

- Equities (+42%): A net +42% are overweight global equities, up from +38% in June. This is slightly above the mean and thus neutral. Over +50% is bearish. A washout low (bullish) would be under +15-20%. More on this indicator here.

- Regions:

- US (-7%): Exposure to the US rose to -7% underweight; it was -19% underweight in May, the lowest since January 2008. For comparison, it was +24% overweight in January.

- Europe (+40%): Exposure to Europe fell to +40% overweight from +46% overweight in June.

- Japan (+37%): Managers are +37% overweight Japan, a small decline from +40% in June. Funds were -20% underweight in December 2012 when the Japanese rally began.

- EEM (-20%): Managers dropped their EEM exposure to -20% underweight. This is the lowest in 16 months.

- Bonds (-60%): A net -60% are now underweight bonds, a small decline from -58% in June. For comparison, they were -38% underweight in May 2013 before the large fall in bond prices.

- Commodities (-22%): Managers commodity exposure decreased to -22% underweight from -11% underweight last month. This is a 6-month low and more than a standard deviation below the long term mean. Low commodity exposure goes in hand with low sentiment towards EEM.

- Macro: 42% expect a stronger global economy over the next 12 months, a 9 month low. January 2014 was 75%, the highest reading in 3 years. This compares to a net -20% in mid-2012, at the start of the current rally.

If you find this post to be valuable, consider visiting a few of our sponsors who have offers that might be relevant to you.