If there is a reason for caution, the risk is mostly short-term (within the next month) and probably not very significant, as explained in this post.

* * *

US equities rose for a 5th month in a row in August, gaining 4-6%. Through the first 8 months of the year, SPX is up 9% while the Nasdaq-100 is up 20% (table from alphatrends.net). Enlarge any chart by clicking on it.

Years like 2018, where the SPX is up between 5-10% through August, have a strong propensity to continue higher to the end of the year. In the past 90 years, there have been 13 similar years: 12 of 13 (92%) closed higher at the end of one of the next 4 months and 11 of 13 (85%) added to their YTD gains through year end (from Nautilus Research).

After a strong start to the year, SPX spent the next 7 months trying to regain its prior high. It finally succeeded a week ago Monday, then added to those highs Tuesday and Wednesday.

On weakness, the January high (2870; top blue line) is the first significant support level (it's also WS2 this week). On more significant weakness, the 2790 area (middle blue line) is major support: this area was the February, March and June high and the July/August low.

That 2790 area is also the rising 20-wma that often defines the longer-term trend in SPX (blue line). The 20-wma has a strong tendency to support lows in the index (arrows).

Stocks tend to keep moving higher after a long consolidation period like that experienced over the past half year. In 18 similar instances since 1954, SPX closed higher 3 months later 83% of the time and 12 months later in all instances except one (94%) with a median gain of 12% (from Ryan Detrick).

Likewise, SPX has closed higher 5 months in a row, a sign of strong upward momentum that normally continues over the subsequent months: SPX closed higher at the end of one of the next 4 months in 23 of 25 instances (92%) and a year later in all but one (96%) by a median of 12% (from Steve Deppe).

The propensity for continued strength is also shown in the following table: after not making a new high in over 120 days, SPX does not typically rollover but instead makes a median of 19 additional new highs over next 100 days (i.e., through the first week in January 2019; from OddStats).

The balance of evidence points to continued strength in US equities over the coming months. That is further supported by the following:

First, the uptrend in US equities is fairly broad. In the past week, the small cap index (RUT), the Nasdaq indices (NDX and COMPQ) and the Russell 3000 (RUA), which comprises 98% of total US market capitalization, all made new ATHs.

Second, both the equal-weight SPX and NDX have made new ATHs in the past week. In other words, if you exclude the FAAMNG companies, the other 99% of SPX and 94% of NDX are also trading at a new high.

Third, for the most part, long term measures of investor sentiment are not overly bullish. Equity fund flows, for example, have been predominately negative since peaking in January. Could equities decline 3-5% in the next few weeks? Sure. Have they peaked for the year? That seems to be very unlikely (from Sentimentrader; to become a subscriber, please use this link).

Fourth, the rise in equities continues to not be driven by those companies doing the most share buybacks on a net basis (from Lisa Abramowicz of Bloomberg).

Finally, the macro economic environment supports the ongoing equity rally. In the past month:

Unemployment claims have fallen to a 49 year low. Historically, claims have started to rise at least 7 months ahead of the next recession (chart below).

Real retail sales made a new ATH, growing 3.4% yoy.

Industrial production (real manufacturing, mining and utility output) made a new ATH with annual growth of 4.2%.

New home sales through July are tracking annual growth of 5% YTD.

Why does any of this matter for the stock market? Equity prices typically fall ahead of the next recession, but the macro indictors highlighted above weaken even earlier and help highlight an oncoming bear market. On balance, these indicators are not hinting at an imminent recession (note blue text). Our monthly economic commentary is here.

Now, it's true that US equities are doing very well while those in Europe, Japan and in emerging markets are, at best, flat on the year. But outperformance by the US has not typically portended calamity: since 1990, this situation has occurred 10 times, with SPX higher 6 months later 80% of the time and 12 months later 100% of the time by an average of 17% (from Ned Davis Research).

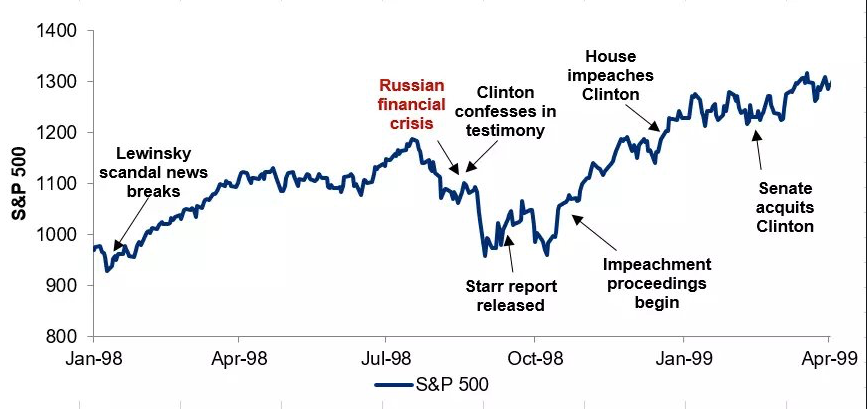

Politics are also an unlikely source of sustained market risk. The Clinton impeachment in 1998 provides an example: the SPX mostly rose throughout and ended the year more than 20% higher (from Barry Ritholtz).

The main market risk appears to be short term.

September has historically been a weak month for equities, especially in mid-term election years. Stocks typically peak early in the month and then begin to rally a month before the election (arrows; from Stock Almanac).

Now, it's true that the typical mid-term pattern has not been followed this year, and that August, which is also seasonally weak, was strong this year. But there are two reasons for caution.

First, short-term measures of investor sentiment are borderline extreme: the 10-day average equity-only put/call ratio is at a level where stocks have often traded sideways to lower over the next several weeks. There were similar readings to today's in both May and June and SPX subsequently gave up 1.5% and 3%, respectively.

Second, new ATHs in August have had a historical tendency to precede weakness in September. There have been 13 years with a new ATH in August and SPX closed September lower in all but two (85%) by a median of 1% (from Steve Deppe).

For reference, the 2790 support level discussed earlier is less 4% lower than the August close.

In summary, US equities have gained every month since April, and are up 9% so far in 2018. Our long term view remains that SPX will move higher by year-end. Risks are mostly short-term.

On the calendar this week is the monthly employment report on Friday (from IBD Investors).

On the calendar this week is the monthly employment report on Friday (from IBD Investors).

If you find this post to be valuable, consider visiting a few of our sponsors who have offers that might be relevant to you.