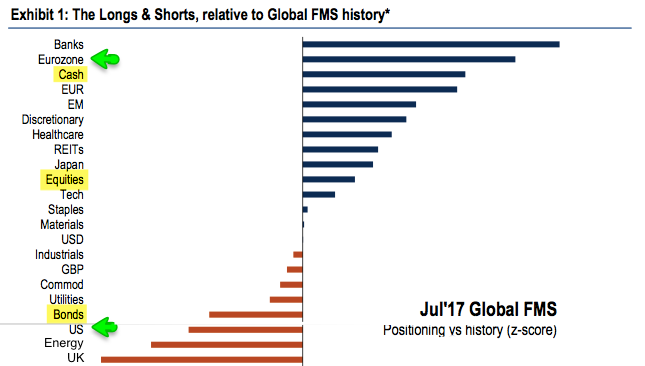

Allocations to US equities dropped to nearly their lowest level since November 2008 in July: this is when US equities usually outperform. In contrast, weightings towards Europe in particular have jumped to levels that suggest this region is likely to underperform. These weightings also suggest that Europe is likely to be the source for any global "risk off' event. Notably, the S&P has outperformed the Europe's STOXX600 by 7% the past two months.

Fund managers remain stubbornly underweight global bonds. Current allocations have often marked a point where yields turn lower and bonds outperform equities.

For the first time in eight months, fund managers are neutral towards the dollar after having considered it overvalued since November. During this time, the dollar has fallen 7%. A headwind to dollar appreciation has dissipated.

* * *

Among the various ways of measuring investor sentiment, the BAML survey of global fund managers is one of the better as the results reflect how managers are allocated in various asset classes. These managers oversee a combined $600b in assets.

The data should be viewed mostly from a contrarian perspective; that is, when equities fall in price, allocations to cash go higher and allocations to equities go lower as investors become bearish, setting up a buy signal. When prices rise, the opposite occurs, setting up a sell signal. We did a recap of this pattern in December 2014 (post).

Let's review the highlights from the past month.

Overall: Relative to history, fund managers are very overweight cash and very underweight bonds. Their equity allocation is modestly overweight. Enlarge any image by clicking on it.

Within equities, the US is significantly underweight while Europe is significantly overweight.

A pure contrarian would overweight US equities relative to Europe and emerging markets, and overweight global bonds relative to a 60-30-10 basket.