Thus, it was not a big surprise that US indices fell this week. For the most part, they are holding above the January highs, the Dow being the exception.

But ex-US markets have again become a mess, characterized by sideways choppiness over the past 6 months or longer. The Dax ended the week at a 4-month low; the FTSE and Nikkei are even worse.

The All World Ex-US index was at a new high a week ago; now it's back in the middle of a 6-month range. This is germane as our 'Scenario 2' has been for US markets to largely carve out a similar pattern for the better part of 2014 (for background, please read post and post).

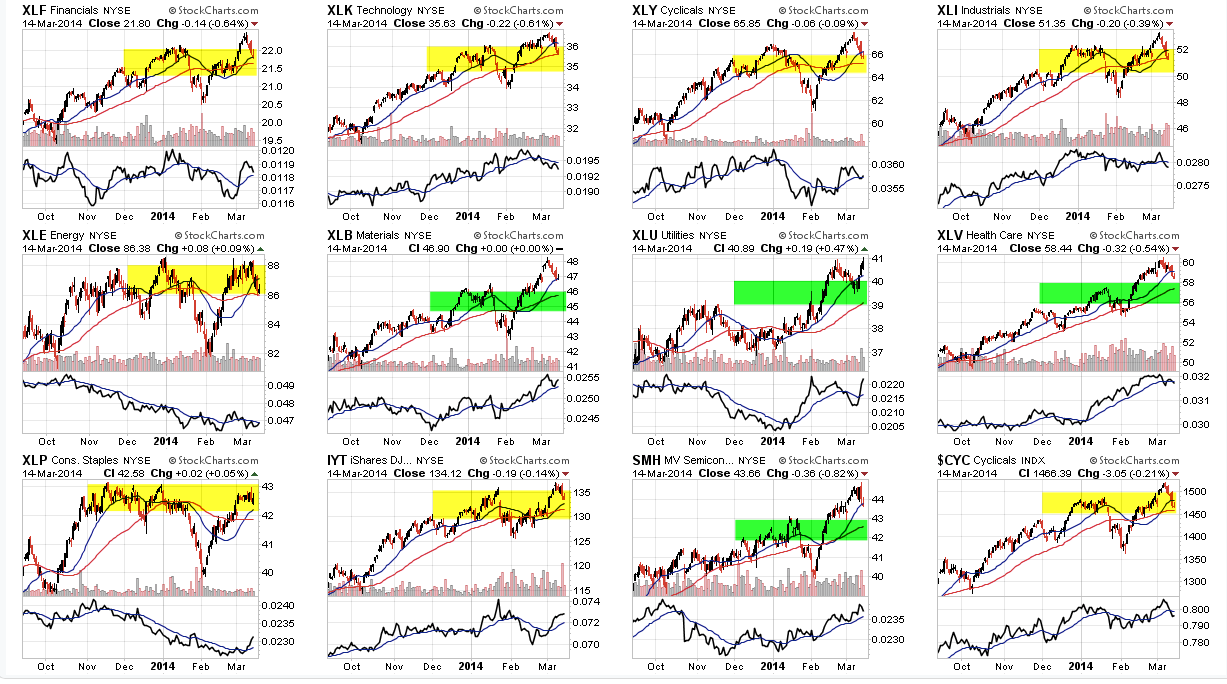

This pattern is being borne out at the sector level. In the US, most sectors fell back into their prior range and have made no net progress over the past 10 weeks. The exceptions are materials, utilities, healthcare and semis. All are holding above their rising 50-dma with a rising 20-dma above. In other words, the short term trend is muddled but the longer term one remains positive.

As weak as the Dow has been, on the weekly timeframe it is still holding in the middle of its Bollinger Band, but barely. A close lower than this has been the precursor to significant lows in the past (yellow). The negative divergence in RSI suggests a bigger washout may be on the way. This coming week is thus key.

As stated, so far the SPX is holding the January highs. However, the index is starting to repeat a familiar pattern: the 13-ema inflects lower (lower panel) and the index heads to the 50-dma, now at 183, over the following weeks (yellow). It also has a strong negative RSI divergence to support this pattern.

A number of factors suggest the markets may first get a short-term bounce before heading lower.

The SPY hourly chart shows a positive RSI divergence, with, again, price ending the week right on key support. Look to the left and note the large supply just below this level. That normally should provide initial price support.

Trin spiked above 2 on Thursday's sell off. When this has occurred after a number of days of selling (solid lines) it has been near at least a short-term low.

Brett Steenbarger similarly shows that when the net number of stocks crossing above/below their 20-dma has reached Friday's levels, the index has risen 1.4% over the next 5 days (post).

March OpX is this coming week; markets tend to go higher, especially if the prior week was down (data is from 1987-2008).

.png)

Lastly, seasonality is typically strong this coming week as well, at least until Friday. Note, however, that the end of March is historically weak (data from Sentimentrader).

A lower low after a bounce seems likely.

Vix is also starting to repeat a familiar pattern. On Thursday, it had its first spike since February. Over the past two years, these have come in pairs, usually a week or two apart (see double lines). The second spike might coincide with SPX's move to its 50-dma.

In the bigger picture, the exuberance that has taken hold of the market is a major headwind to upside progress. A few more examples to add to those discussed last week follow (read the others here).

Despite the weakness in the market this week, retail investors reduced cash and increased their equity holdings. The ratio of these two assets reached a new 13-year high. Remarkable.

At the same time, Mark Hulbert notes that corporate officers are dumping stocks to a degree not seen in almost 25 years; greater than in either 2007 or in early 2011 (here). So, net, historically 'smart money' seems to be selling the rally to historically 'dumb money.'

The number of money-losing IPOs is spiking to February 2000 levels (data from Sentimentrader). As David Schawel notes, there have been 18 biotech IPO's in the last six months, up an average of 74% with 7 up 100% or more.

There is a dash for trash taking place as investors buy the most speculative penny stocks to a degree not seen since before last May's peak in the market (data from Sentimentrader).

Jeff Gundlach sounded a warning on the exuberance in the high yield market: “There's no way for prices to go up at this point. The average junk bond yields just 5.3% and trades above 104 cents on the dollar, higher than the 103 level at which many bonds can be called by their issuers".

Investor exuberance is most evident in small cap stocks. Since the 2009 low, SPX is up 182%, NDX is 245% but RUT is up most of all, by a whopping 254%. As a result, the index is hitting a 14 year trend line.

MKM Partners note that the index is now more than 40% above its 200-dma, the highest since March 2000. "Over the last 30 years, the forward returns for the RUT three months out when it closes 40% or more above this reference point have been negative 94% of the time, averaging a 7% decline."

Ryan Detrick further crunched these numbers. The RUT is positive 3-months and 12-months later less than 15% of the time with median 1-year returns of minus 16%.

These numbers also fit the fundamentals. Valuations on the index are higher than at any time since the 1970s. The forward returns over the following year at prior extremes are minus 20%.

Given all of this, it is perhaps not surprising that treasuries continue to outperform equities so far in 2014. 10 year treasury yields sank to 2.65% on Friday. Recall that the 50-dma (blue) has been a dividing line many times in the recent past (circles). It closed on it last week, then sold off this week. They are now below their 200-dma once again in March.

Our weekly summary table follows: